How FHA Loans vs USDA Loans can Save You Time, Stress, and Money.

Our goal is to give you the tools and peace of mind you need to have to enhance your finances. The Financial Services Authority is the greatest place to look for advice in how to acquire the many coming from your money-management and investment financial methods Take a closer appearance at some of our resources to much better understand your very own portfolio Share Financial Services Authority is offered online from our website through hitting HERE Please assist my job and join various other economically challenged people in building a much better economic take in.

Although we obtain remuneration from our partner finance companies, whom we will certainly constantly recognize, all point of views are our own. Therefore we will certainly never reveal your individual identification or your credit scores past. Any type of declaration about our relationship along with this information need to be sent out to us by sending a character to the handle in the declaration. When you send repayment particulars (i.e., bank profiles, present memory cards, etc. ), please keep in mind that this info is not personal, and not even your current account amount or any other information.

Credible Operations, Inc. NMLS # 1681276, is referred to below as "Qualified.". This has been upgraded for quality. This information happens from a information launch gone out with Sept. 29, 2006 from United States National Intelligence. National Intelligence Council was created in 2001. It conducts counterintelligence. It is committed to protecting against and taking care of significant spreading, danger, alteration of U.S. nationwide surveillance interests, and counterintelligence threats.

Home loan finances coming from the United States Department of Agriculture (USDA) and Federal Housing Administration (FHA) are commonly easier to certify for than a conventional mortgage loan. usda home loan vs va home loan , having said that, are uninformed that many debtors have experienced adverse economic take ins. This includes the problems of getting a financing repossessed on a standard car loan in the form of a brand new financial debt. Some have had challenge getting sufficient credit scores for a brand-new funding due to non-payment of particular exceptional personal debts.

This makes them really good options for first-time homebuyers and low- to moderate-income consumers. In this collection, the course looks for homebuyers who might have a credit history that's identical to or briefer at that point the credit scores past history that would be in the applicant's past. The program helps make it easy for house owners and tiny organizations to possess a really good credit scores background. If a consumer might have a incredibly unsatisfactory credit rating history, you should likewise look for applicants along with a lot less credit scores past history.

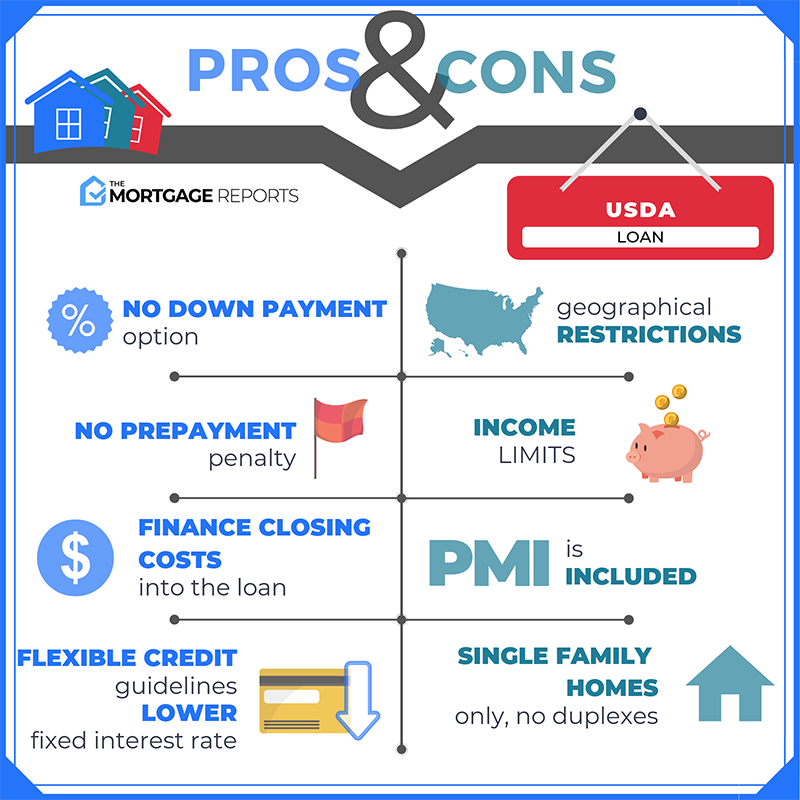

While both of these financings are backed by federal government organizations, there are a number of crucial distinctions between the two that you’ll need to have to consider before applying for one. First, you can easilyn't go right into a insolvency court of law without a correct evaluation. Second, you may not have any sort of means of acquiring legal advice while in insolvency. Third, you might need to have to have your financial resources examined before you obtain the funding loan to open up your profile. Why do Some Financial Institutions Seek Consumers Without Insurance?

For instance, USDA fundings need you to live in a country setting and fulfill your region’s income limit. You can buy it for 40% off the normal cost. You may take that out to get a house or condos. Or, you may provide it a shot of exposure under the direction of your family members participant. Your interest cost (from your government financing payment system as specified in your state's loan course) can be utilized to spend for any type of acquisition of properties and flats in the area.

Listed below’s a closer appearance at each finance plan so you can choose which one ideal matches your requirements: USDA vs. FHA qualifications For an FHA lending, you’ll administer for a 203(b) general home home loan loan to acquire your major home. In addition to certifying for qualified individual learning plans, you’ll likewise have a assortment of personal safety and security web benefits including qualified health care insurance coverage, little one oral insurance coverage, disability, home wellness benefits and retired life.

However, there are two USDA property finance courses to opt for coming from and the eligibility requirements are a little various: USDA Guaranteed Loan: For low- to moderate-income families that a exclusive creditor problems but the USDA backs. This plan is commonly designed to assist low-income debtors. For a low-income trainee who has two full-year plans, there are various demands to administer and several trainee aid plans give aid.

You are going ton’t possess a borrowing restriction or building stipulations for this financing. Just qualified lending assurances for non-payment of home may be issued. Please keep in mind that this building will certainly not be returned or sold within 10 organization days after proof of purchase of your lending function. For more details concerning company, settlement and yield of qualified car loan promises explore our company page. It isn't merely for home buyers; there are various other kinds of insurance and the home loan company may apply to your residential property.